MAINE, USA — State leaders tasked with reviewing Maine’s preparations and responses to climate change-fueled natural disasters are at a crossroads.

While Maine has seen seven federal disaster declarations for severe storms and flooding in the past three years, statewide enrollment in federally-backed flood insurance policies is dwindling.

Public infrastructure has been repeatedly damaged, including the coast’s working waterfronts, and the state has been reliant on federal disaster assistance to rebuild and strengthen damaged infrastructure.

At a meeting earlier this month, members of the state Infrastructure Rebuilding and Resilience Commission wondered whether a public insurance option offered by the state could protect both the uninsured and the state’s own public infrastructure.

“It’s the only way I can think of that actually provides a permanent stream of funding … to respond … to disasters as they occur and the need for increased resilience,” said Charlie Colgan, an economist and policy analyst at the University of Southern Maine.

Climate resilience, Colgan said, “is going to have to come mostly from our own resources.”

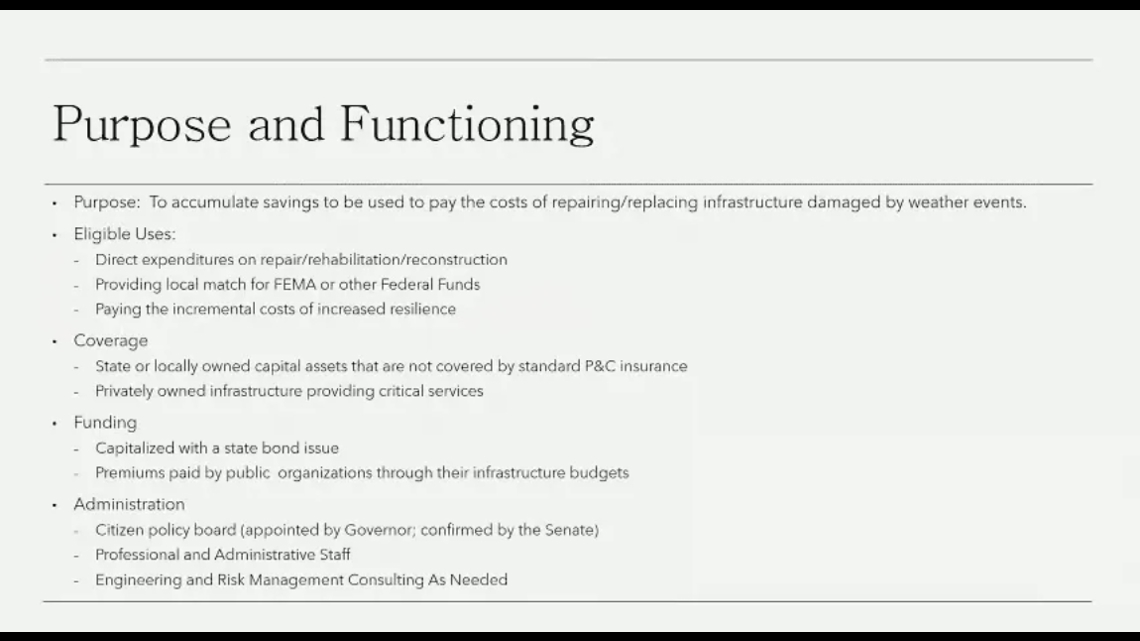

Colgan’s proposal, which he presented during the meeting on Sept. 4, includes a public insurance model jump-started by a state bond.

What would happen next is less clear. The insurance program, as Colgan envisions it, would at first be open only to public entities, like municipalities, who would pay into the pool and draw money after disasters.

Payouts could also cover funding obligations for federal grants and fund general resilience projects, like upsizing culverts.

If extended beyond the public domain, Colgan imagines the program could also provide an additional layer of protection for Maine property owners — acting as a low-cost insurance option that would fill the gaps of federally-backed flood insurance.

There are other publicly funded insurance programs in the U.S., including the Citizens Property Insurance Corporation. The non-profit public insurance company was formed by the Florida state legislature in 2002 as an insurer of last resort but has been plagued by complaints from policyholders.

The idea for a publicly-funded option in Maine energized fellow commission members when Colgan presented it in early September, shortly after the group painted a grim picture of the state’s current insurance coverage.

Only 1.3 percent of all homes and buildings in Maine are covered under the National Flood Insurance Program, a number that has declined by 25 to 30 percent since 2009, according to Peter Slovinsky with the Maine Geological Survey.

Meanwhile, Mainers who do have flood insurance are filing more and more claims. Over the past 10 years, Mainers filed a total of 443 claims, paying out a sum of $16 million, according to Maine Bureau of Insurance Superintendent Bob Carey.

Nearly half of those claims came from the past year alone, Carey said, accounting for 164 claims totaling roughly $8 million.

Commission members only had vague ideas of what could be causing the decline in the number of homes and buildings covered under the National Flood Insurance Program. More houses could be owned outright, Slovinsky suggested, meaning that homeowners would not be required to purchase a flood insurance policy like they would with most federally-backed mortgages.

Many who aren’t required to have flood insurance are opting out of buying coverage because annual premiums are rising or because they don’t trust that the payout will be worth the premium. Several flood victims who filed claims after last winter’s flooding have told The Monitor that the payout hasn’t always been worth the cost.

“I mean, if you think for the past six years, we’ve spent $40,000 in flood insurance to have not covered anything,” said Gardiner business owner Stacy Caron back in January, a month after her family’s pizza parlor was wrecked by flooding from the Kennebec River.

For comparison, flood insurance policies nationwide paid out an average of $44,401 per claim in 2021, according to online insurance marketplace Policygenius.

Colgan also tied Maine’s low participation rates to insurance lapses that the commission has seen along the coast.

Privately-owned wharfs in places like Stonington, for example, are the spine of Maine’s coastal economy but don’t necessarily have the insurance coverage they need to recover on their own after disasters like this January’s flooding, Colgan said.

“A lot of the working waterfront facilities that were destroyed are private utilities, but provide essential public services,” said Dan Tishman, commission co-chair and chairman of Tishman Realty & Construction.

Linda Nelson, chair of the commission and Stonington’s economic and community development director, estimated that only a little more than a dozen Stonington property owners had flood insurance policies, which didn’t provide the money needed to build back resiliently.

“The things they thought were going to be covered by [flood insurance] somehow weren’t possibly covered by [flood insurance],” Nelson said.

That’s where Nelson thought Colgan’s public insurance model could come into play, bridging the gap between simply rebuilding at-risk infrastructure and strengthening or relocating it to weather future climate change-induced storms.

“A private owner might decide, ‘I can afford 40 grand for insurance, but I can’t afford 200 grand, so I’m going to look for a layered approach,’” said Dan Tishman, commission co-chair and chairman of Tishman Realty & Construction.

They then “would be willing to pay into the layered approach if it was less expensive than trying to buy it through the capital markets,” Tishman added, building the insurance pool in the process and bringing others’ premiums down.

Commission members seemed excited with the idea, even if it was only in its infancy.

The state’s dawdling insurance adoption and mounting costs for resilience projects are a huge concern, and the commission has to come up with concrete policy suggestions and funding sources by November.

Members suggested other, more actionable ideas to address the insurance issue; like funding a study to determine why flood insurance participation is falling, increasing municipal participation in a federal program that brings down flood insurance rates, and general outreach.

But the insurance model was the focus of conversation, especially when members thought of the daunting funding needs for resilience projects.

Colgan said that the state was in a relatively strong financial position during last winter’s catastrophic flooding, but the $60 million that Gov. Janet Mills specifically dedicated to resilience and recovery projects in this year’s supplemental budget won’t always be there, nor is it enough to counter the severe storms increasing in frequency and intensity.

“How do we avoid not only the twin risks of the climate and weather disasters, but also the economy and the ability to have the resources to scratch the surface of recovery?” Colgan asked.

This story was originally published by The Maine Monitor, a nonprofit and nonpartisan news organization. To get regular coverage from the Monitor, sign up for a free Monitor newsletter here.